The 33kV Wall

The energy transition is creating a brief opening in one of the hardest industrial sectors to crack. Can a new generation of Indian companies build lasting capabilities before the window closes?

15 June 2026· 5 min read

TL;DR

The global energy transition presents a unique, fleeting opportunity for a new generation of Indian companies to break into the historically impenetrable power electronics sector. Traditionally dominated by multinational giants due to decades of accumulated operating experience and trust, the shift towards dynamic renewable energy grids, battery storage, and EV charging is creating demand for innovative solutions where incumbents hold fewer inherent advantages.

India's monumental grid redesign offers a critical proving ground. However, a significant barrier—the "33kV wall"—lies in overcoming the experiential gap, requiring Indian firms to rapidly cultivate deep capabilities, gather extensive operational data, and earn customer trust. Companies like InPhase Power Technologies, by building their own testing facilities, exemplify this proactive approach, highlighting the urgent need for Indian companies to establish lasting capabilities before this critical window of opportunity closes.

When InPhase Power Technologies began building medium-voltage power electronics, it ran into a problem that had nothing to do with technology.

The company needed to test its products before customers would buy them. But it discovered that no suitable testing facility existed in India for what it was trying to build.

So it built one.

That decision captures both the promise and the challenge facing a new generation of Indian power electronics companies.

For decades, the most valuable layer of the sector has been dominated by multinational giants such as Hitachi, Siemens and GE. Their advantage was never just capital. It was decades of accumulated operating experience, installed systems, certification records and customer trust.

Breaking into that world has historically been close to impossible.

Yet the energy transition is beginning to create opportunities in parts of the market where those advantages matter less than they once did.

As renewable energy, battery storage, EV charging and industrial automation spread through the economy, electricity is becoming more dynamic, more complex and more difficult to manage. That, in turn, is creating demand for a new generation of power electronics.

For the first time in decades, a small group of Indian companies believes it has a chance to build globally relevant businesses in this space.

The opportunity is real.

The window may not remain open for long.

Few technology markets move as slowly as electricity. Customers buy equipment that is expected to work reliably for decades, not years. Trust is earned through operating history, certifications and field performance, not product launches.

For a hundred years, the electrical grid was built around a simple assumption: power flows one way, from large, centralised plants to passive consumers, in predictable volumes that engineers could plan around.

Renewable energy changed that equation. Power now flows in multiple directions, in unpredictable volumes, from many distributed sources—rooftop panels, wind farms and solar plants owned by commercial customers—back into the system. Grids everywhere are discovering that the infrastructure built for the old world cannot simply be upgraded to handle the new one. It has to be redesigned.

India will spend the next two decades building one of the largest such redesigns in history. Much of it will be supplied by the same foreign companies that have dominated the sector for decades. But the redesign is also creating new categories where incumbents have fewer advantages to lean on. In these emerging segments, the rules are still being written.

The Advantage That Can’t Be Bought

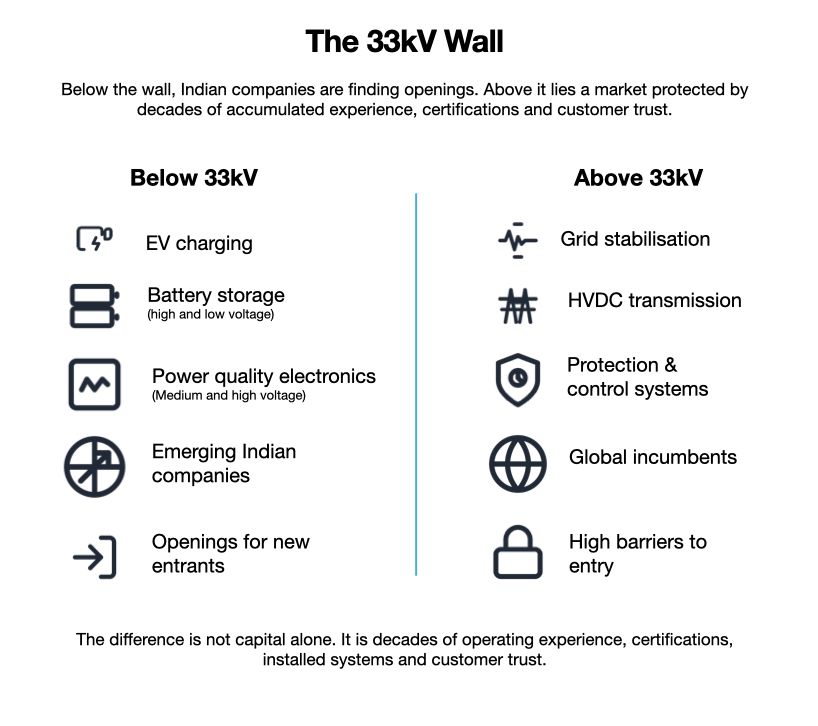

To understand why this opportunity is unusual, it helps to understand the barrier that has historically kept most Indian companies out.

Power electronics, the active layer that converts, controls and stabilises electricity, is where complexity—and barriers to entry—rise sharply with voltage. The table below shows where the market divides and where the wall begins.

The wall sits at 33kV.

Indian companies have built successful power equipment businesses in categories such as transformers and reactors, though often only after decades of persistence and competition with global incumbents. Active power electronics has proved far harder to crack.

The barriers are not financial. They are experiential. Hitachi and Siemens’ control software carries decades of grid fault data from systems operating across the world. An Indian company attempting to build a 220 kV grid stabilisation system (known in the industry as a STATCOM) is not just building hardware. It is trying to compress four decades of institutional learning into five years of product development. That gap cannot be funded away.

The certification system creates a Catch-22 situation. To win a major utility contract, a company needs a reference installation. But to secure a reference installation, it often needs the credibility that comes from already having one. The companies that eventually broke through, Quality Power in HV reactors and TARIL in power transformers, did so in passive components over multiple decades, not in active electronics.

Companies invest in product development, build engineering teams and spend years navigating certification processes. By the time approvals arrive, customer requirements may have shifted, technologies may have evolved and competitors may have moved ahead.

The challenge is not simply that the cycle is long.

It is that nobody can be entirely sure where the cycle will end.

This is not just a long cycle. It is a cycle with an uncertain destination.

Betting Before the Market Exists

The companies attempting to build in this space are not taking on Hitachi or Siemens head-on. Most are looking for openings in markets that are still small, evolving or poorly served. The common thread is that each is making a bet long before the outcome is obvious.

InPhase is betting on a customer problem.

AmpereHour is betting on regulation.

Dynolt is betting on a technology shift.

InPhase is betting that power-quality problems will become unavoidable as factories add more solar and automation.

AmpereHour made a different bet: that storage would eventually become an essential part of the electricity system.

Dynolt is betting on something else entirely: that a new semiconductor cycle will briefly level the playing field.

The specifics differ. But all three companies are trying to do the same thing: build capabilities before the market fully forms and before larger competitors decide it is worth entering. And because the domestic market is still nascent, success will likely require building for global markets from the outset.

These are still early bets. The sector is only beginning to attract venture capital and growth funding. AmpereHour is backed by Avaana Capital, Dynolt by Transition VC, while others such as Enerzolve and Ergon Labs have raised seed capital. But investors are funding possibilities, not proven outcomes. Larger pools of capital will arrive only if the current generation can demonstrate that these businesses can survive long development cycles, certification hurdles and global competition.

The Clock is Running

Part of the opportunity exists because some of the industry's largest players are currently focused elsewhere.

That will not last forever.

The length of the window varies by category. In some segments, Indian companies are racing against established global incumbents. In others, they are racing against Chinese manufacturers or against the economics of the market itself. The challenge looks different in each case.

In commercial and industrial (C&I) power electronics, the race is against incumbents.

For the C&I segment, Indian companies may have three to five years before MNC incumbents decide the market is large enough to pursue with products tailored to the market and more aggressive pricing. Hitachi, Siemens and GE are not ignoring this space; they are deprioritising it as their order books are full of grid-related orders.

When C&I becomes material to a global MNC's India P&L, they will enter with service networks, balance sheets, and brand equity that a six-year-old startup cannot match. At the lower end, Chinese pressure is already present. Sungrow, Growatt and Huawei are already deeply embedded in India's solar and power electronics ecosystem, with scale and cost positions domestic manufacturers cannot match at equivalent volumes.

In EV power electronics, the race is against technology cycles.

For EV power electronics, the timelines are longer and the capital requirements higher: seven to eight years of product development, large upfront investments, and the ability to sell globally from day one. The mitigating factor is that technology itself is changing. When an industry moves from one generation of technology to another, old advantages matter a little less and new entrants get a chance to catch up. That is what companies in this space are betting on.

In battery storage, the race is against economics. For storage, rapid growth does not automatically imply attractive economics. Falling tariffs, aggressive bidding and uncertainty around long-term revenue streams have already led to project cancellations and financing concerns. The pressure may ultimately shift value toward the electronics and software layers that maximise asset utilisation, but only if the sector can attract enough capital to get there.

Different categories face different pressures. But they all point to the same question: can today's startups build enough capability, customer trust and installed base before the market becomes significantly harder to enter?

What could extend the window is a combination of two factors. Products designed for Indian conditions from the ground up carry an inherent advantage that imported alternatives cannot easily replicate. And localisation mandates, as and when they are implemented, add a structural tailwind. Together, these could keep the window open long enough for the current generation to build the installed base and certifications that turn a first-mover position into a durable one.

What the Window Requires

India's energy transition is creating one of the largest industrial procurement opportunities of the next two decades. At its centre sits the active electronics layer—the systems that control, convert and stabilise power. Today, that layer is supplied overwhelmingly by foreign companies.

India's grid will be built. The procurement will happen.

The question is whether the order books in 2035 contain any Indian names that did not exist ten years earlier.

For the first time, the capital, the founders and the product categories exist to make that possible.

The window is open.

Nobody knows for how long.

Join the conversation

Bharti Krishnan

Founder | Finetrain

Bharti Krishnan, CFA, is the founder of Finetrain, where she works with climate startups on raising equity, debt, and grants. Her work sits at the intersection of finance and climate tech across energy, water, and materials. She spends most of her time meeting founders and helping them think through capital decisions.

Beyond the noise is the signal.

FF Insights: Sharpen your edge, Monday–Friday.

FF Life: Culture, ideas and perspectives you won't find elsewhere — Saturday.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Loading comments...

More by Bharti Krishnan

Readers also liked

·FF Life

The Happiness We Keep Postponing

A reflection on joy, and why the ordinary day may be enough

HC

Haresh Chawla

Investor | Entrepreneur

The Happiness We Keep Postponing

A reflection on joy, and why the ordinary day may be enough

Investor | Entrepreneur

·Leadership & Organisation

The Blind Spots of India Inc

Disability inclusion, leadership imagination, and the limits of intent

SS

NJ

Subhashis Sinha & Nikunj Kumar Jain

The Blind Spots of India Inc

Disability inclusion, leadership imagination, and the limits of intent

Subhashis Sinha & Nikunj Kumar Jain

·Artificial Intelligence

India’s AI Gambit: The Choices That Will Define Power

Speed is not strategy. The real battle is over sovereignty, science and state capacity

FF

Founding Fuel

India’s AI Gambit: The Choices That Will Define Power

Speed is not strategy. The real battle is over sovereignty, science and state capacity

Explore more

Dive into other themes from our network.